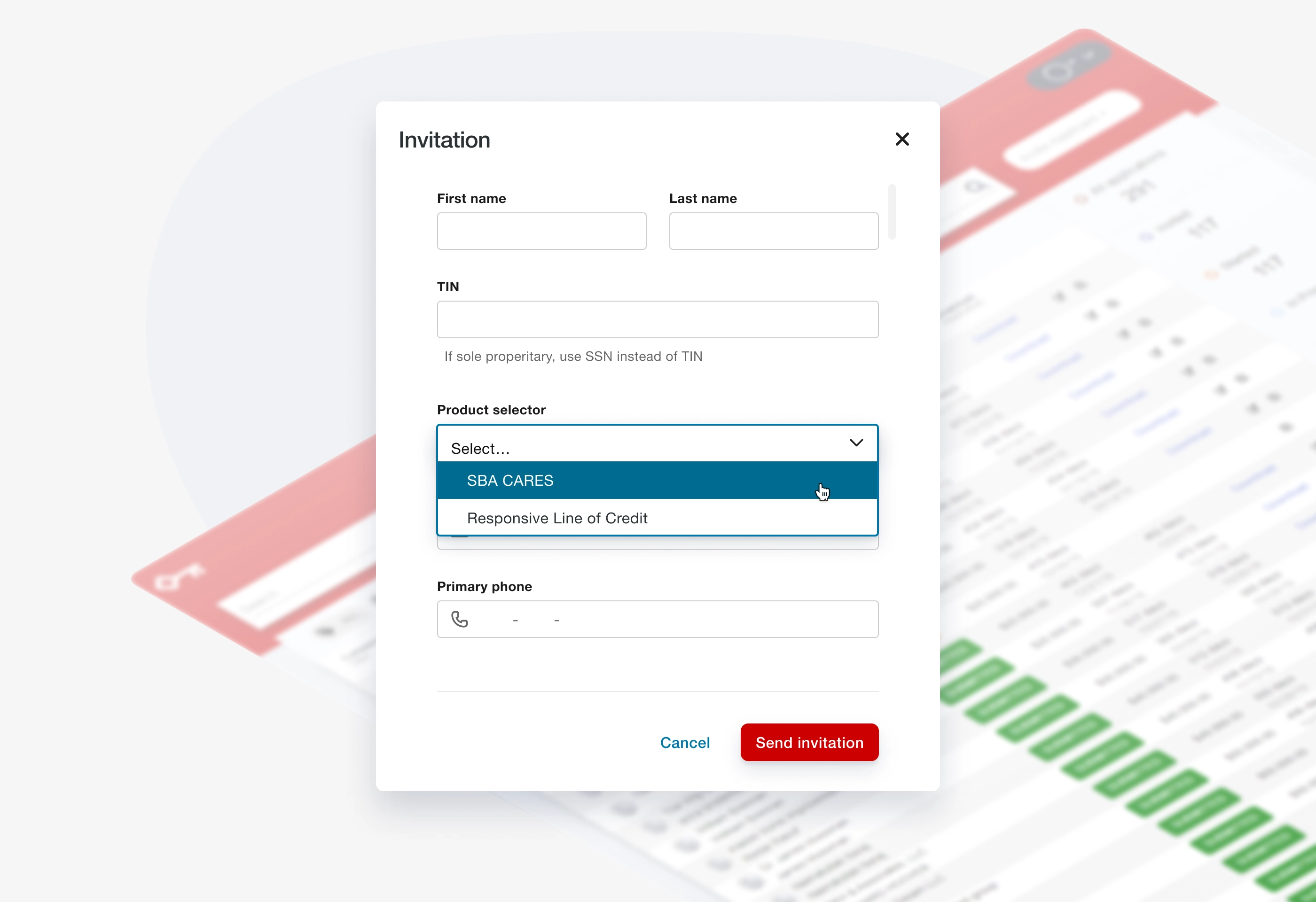

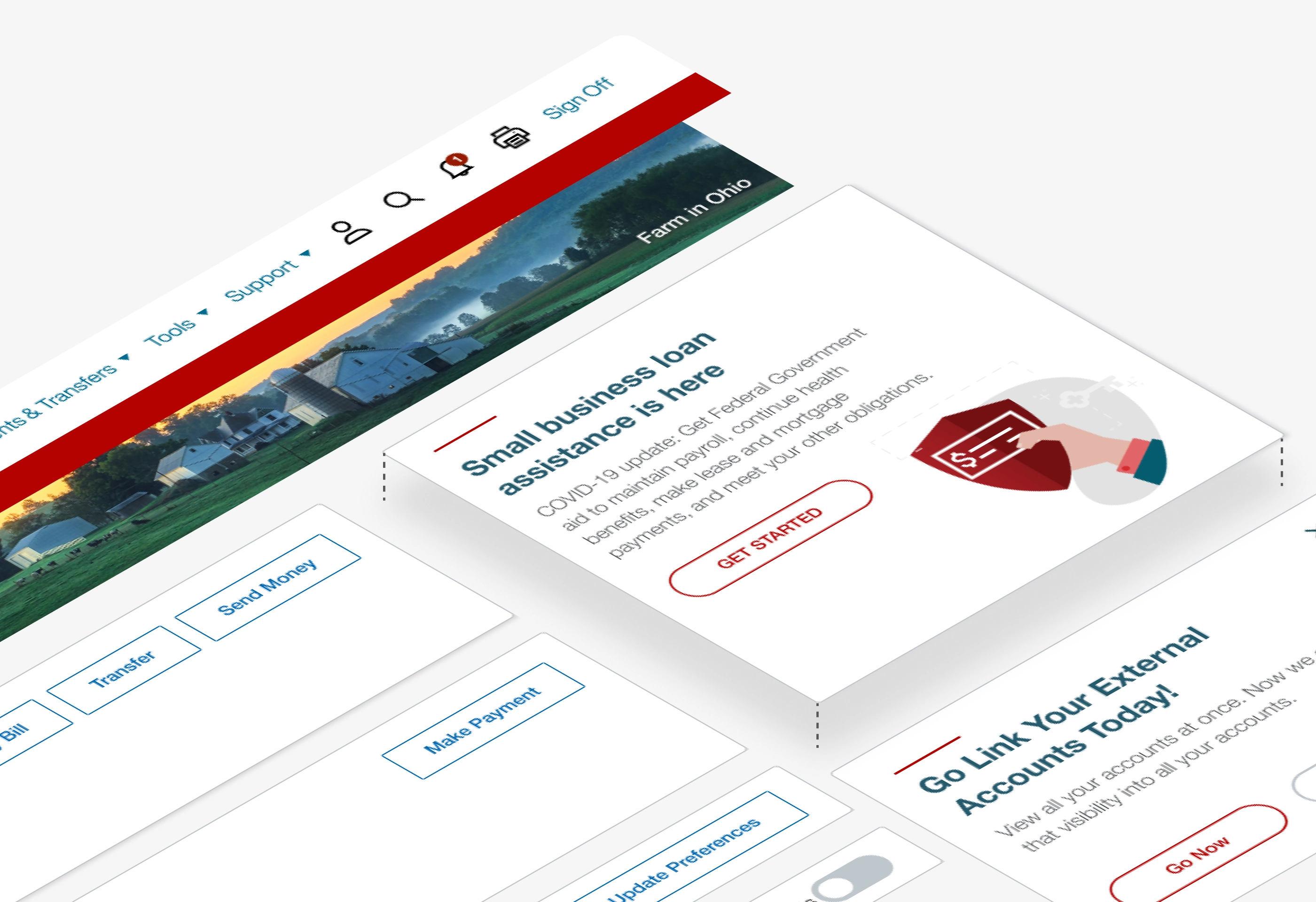

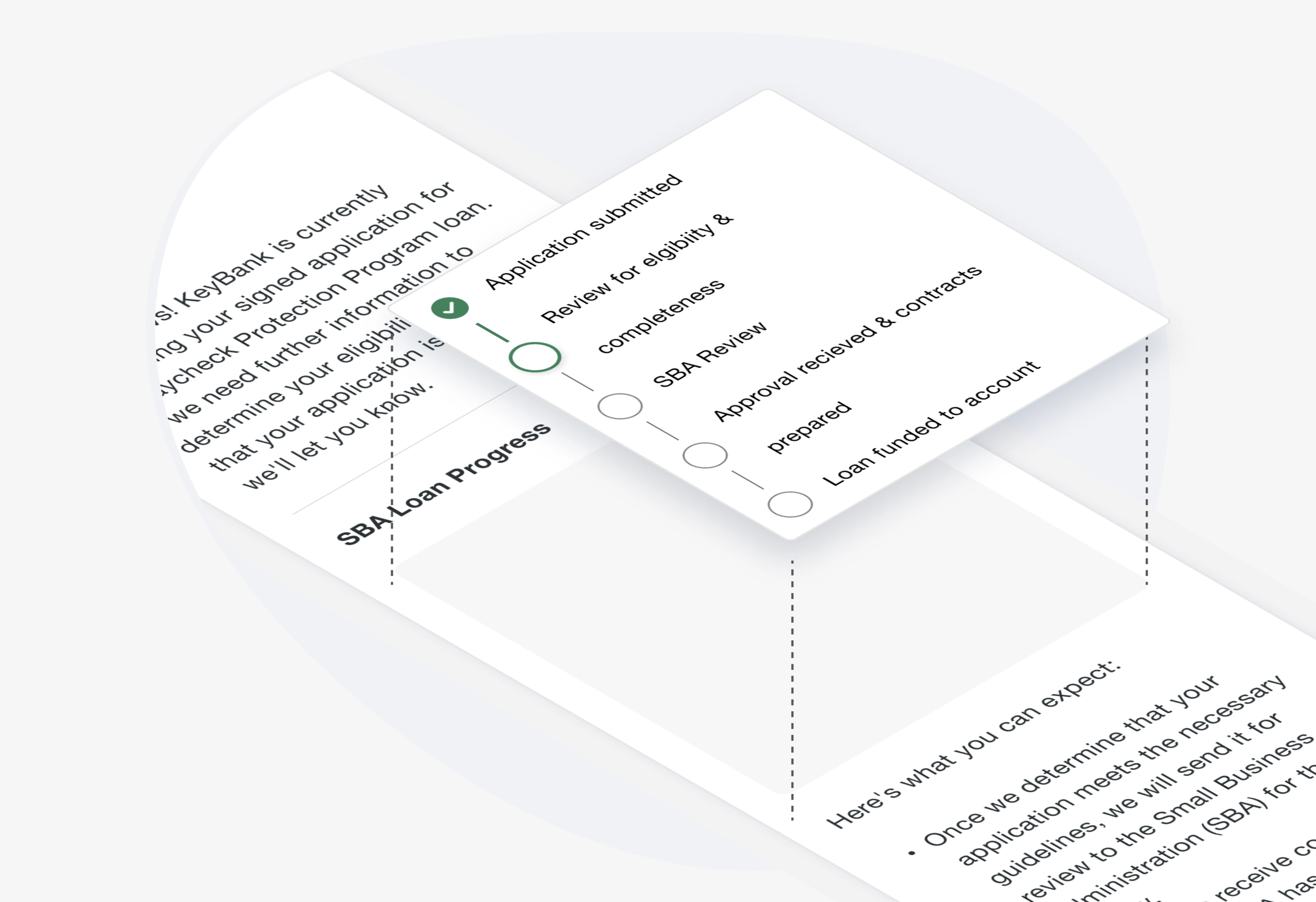

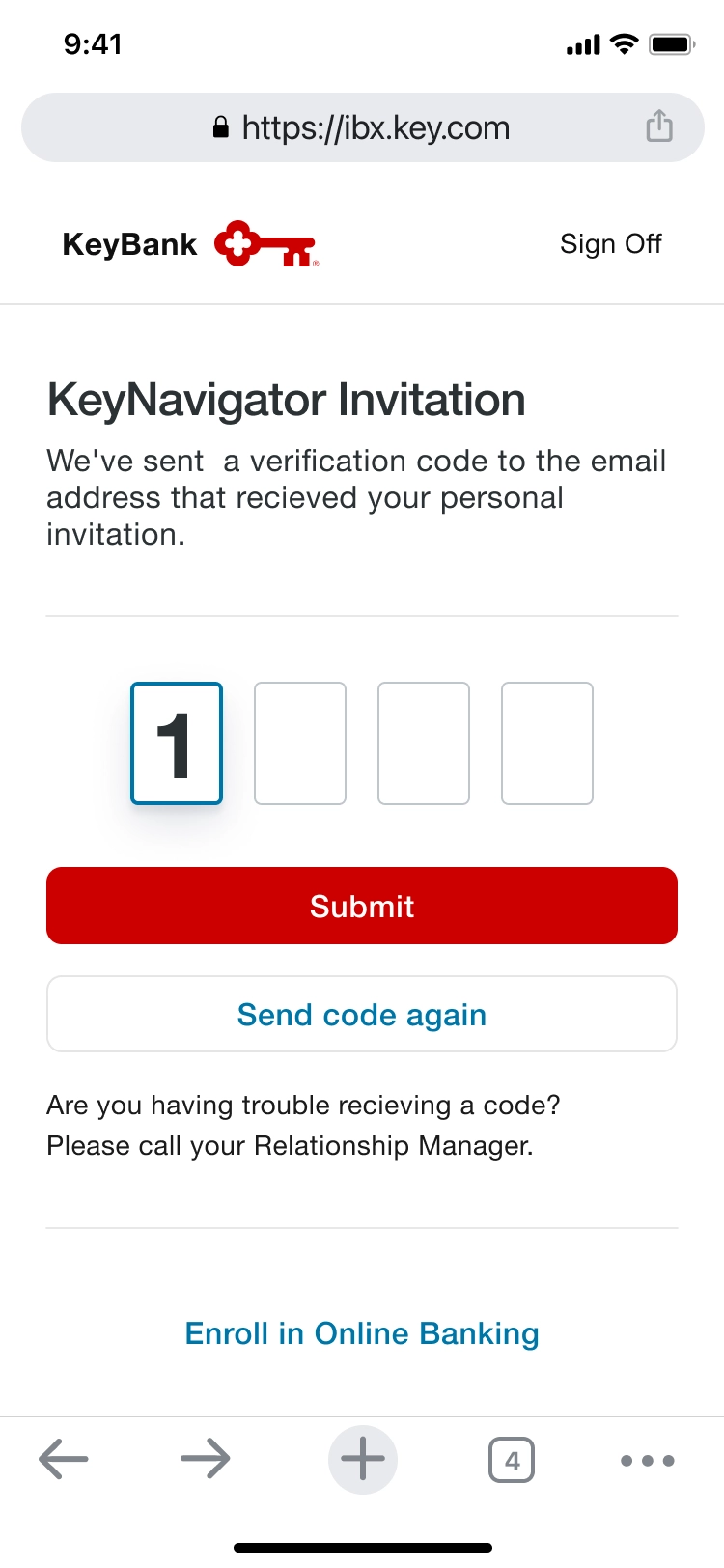

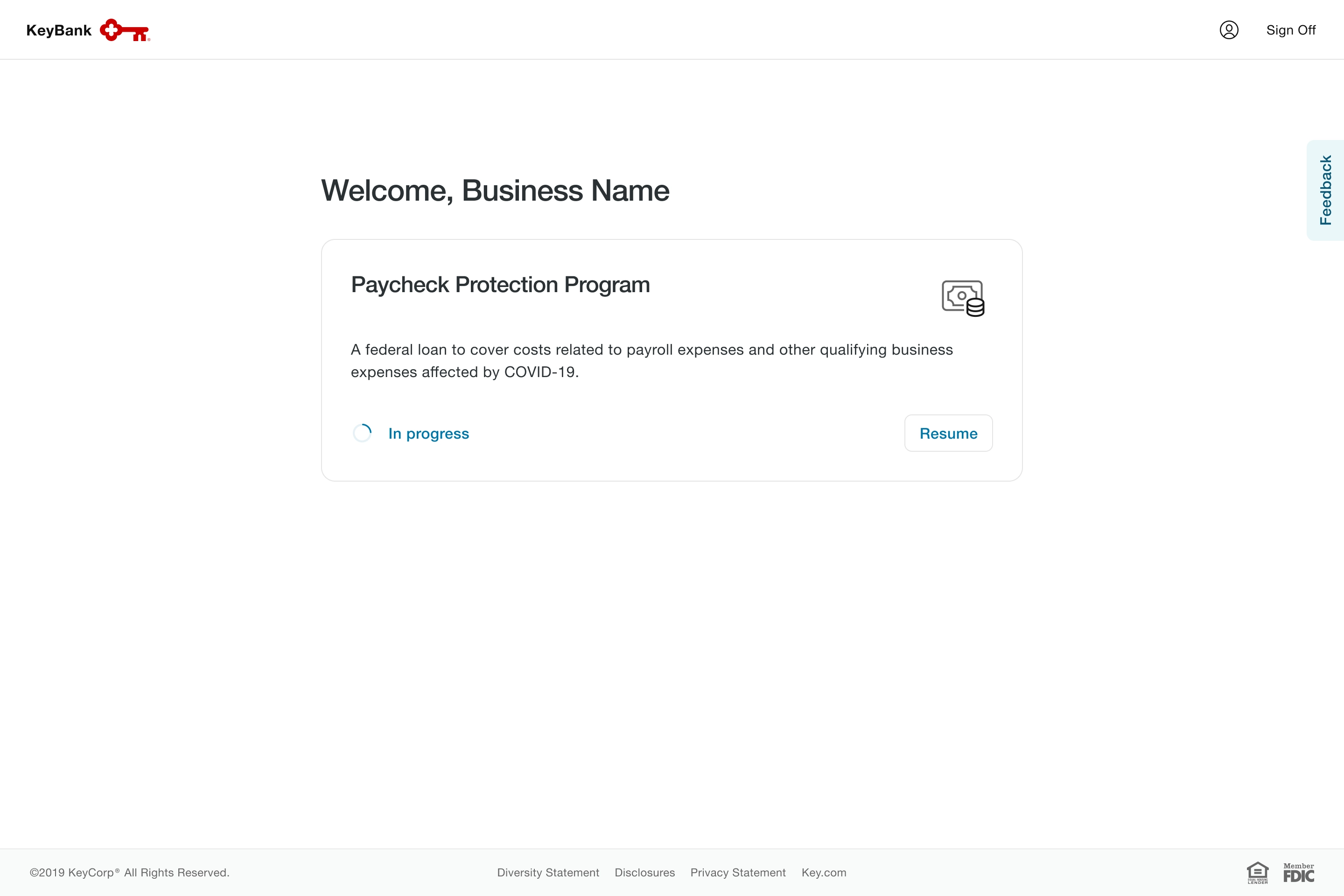

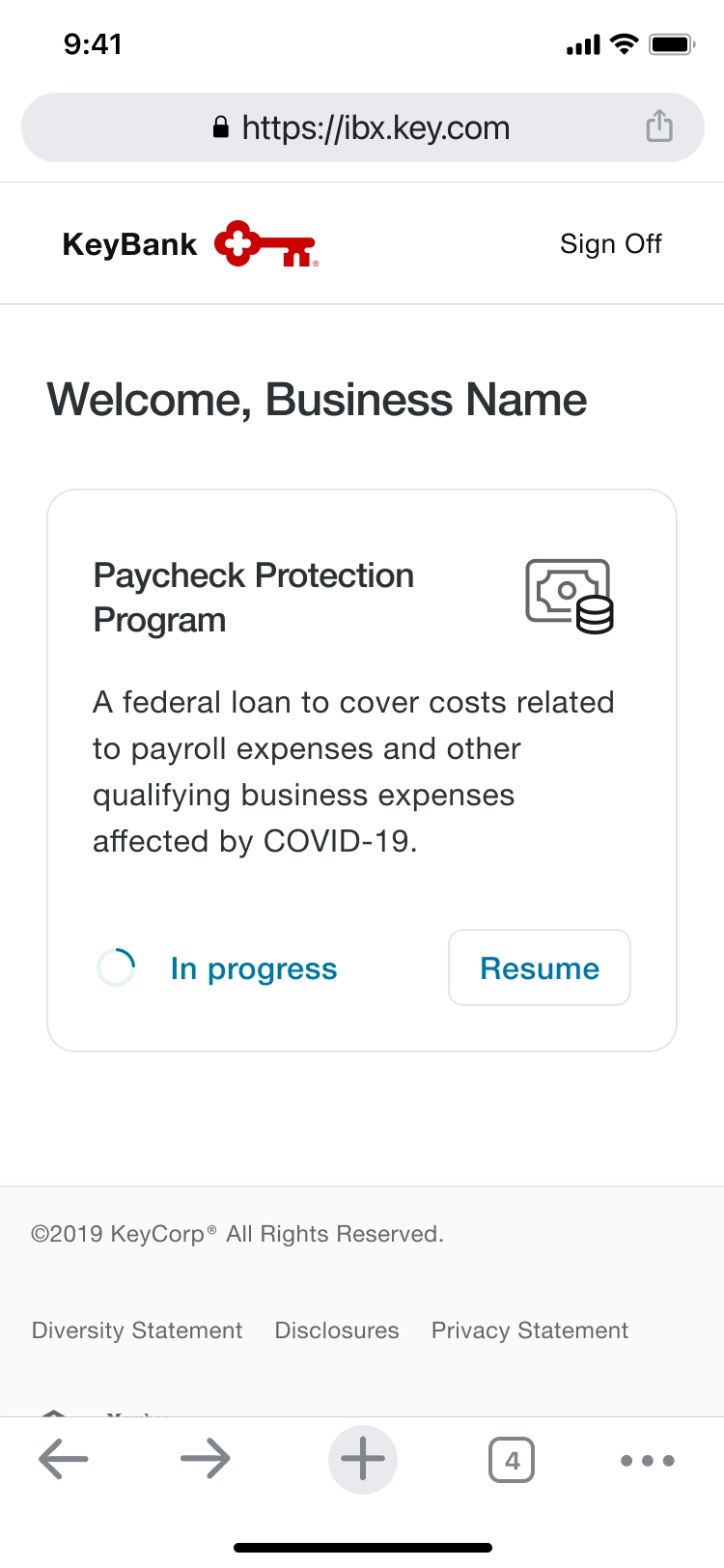

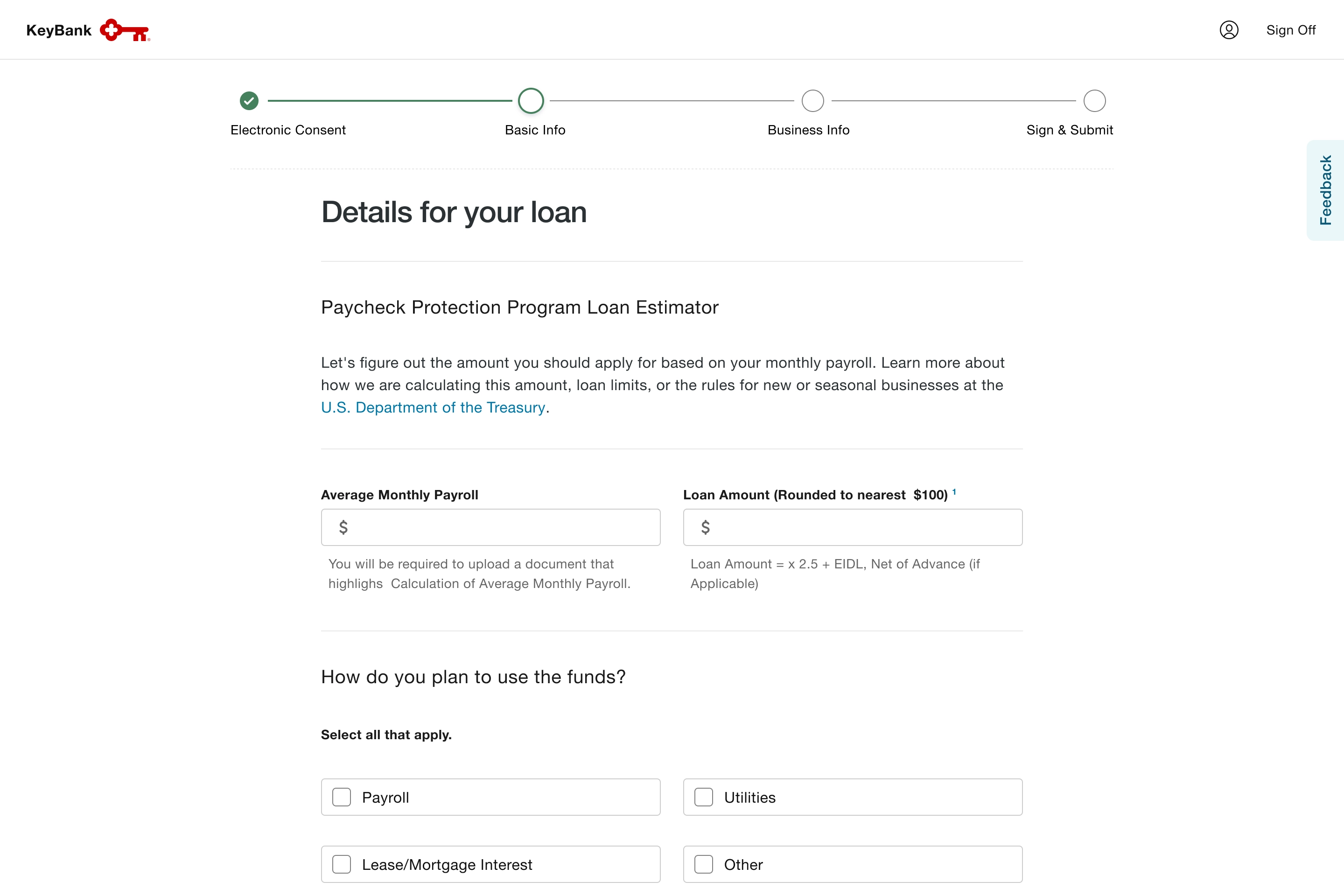

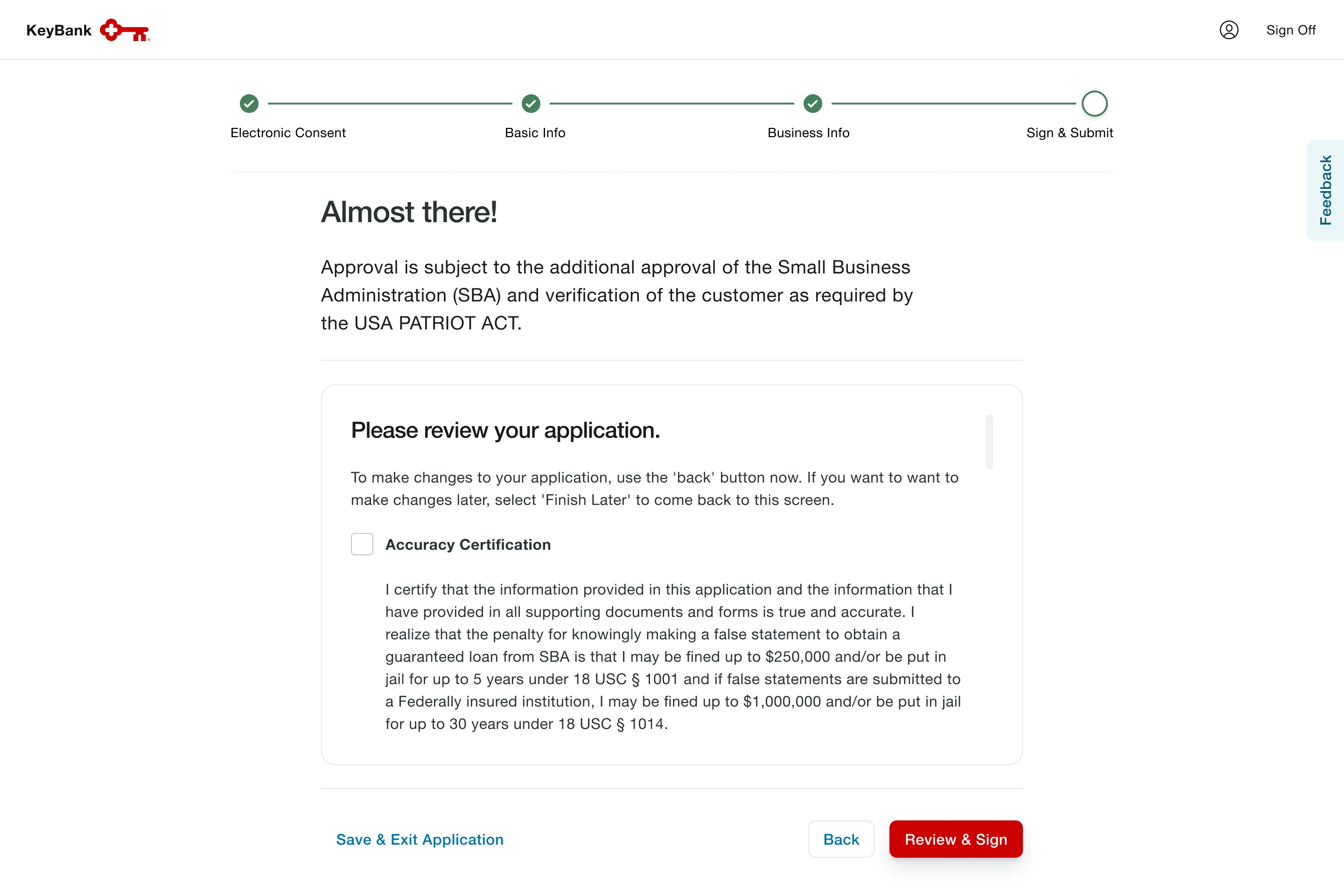

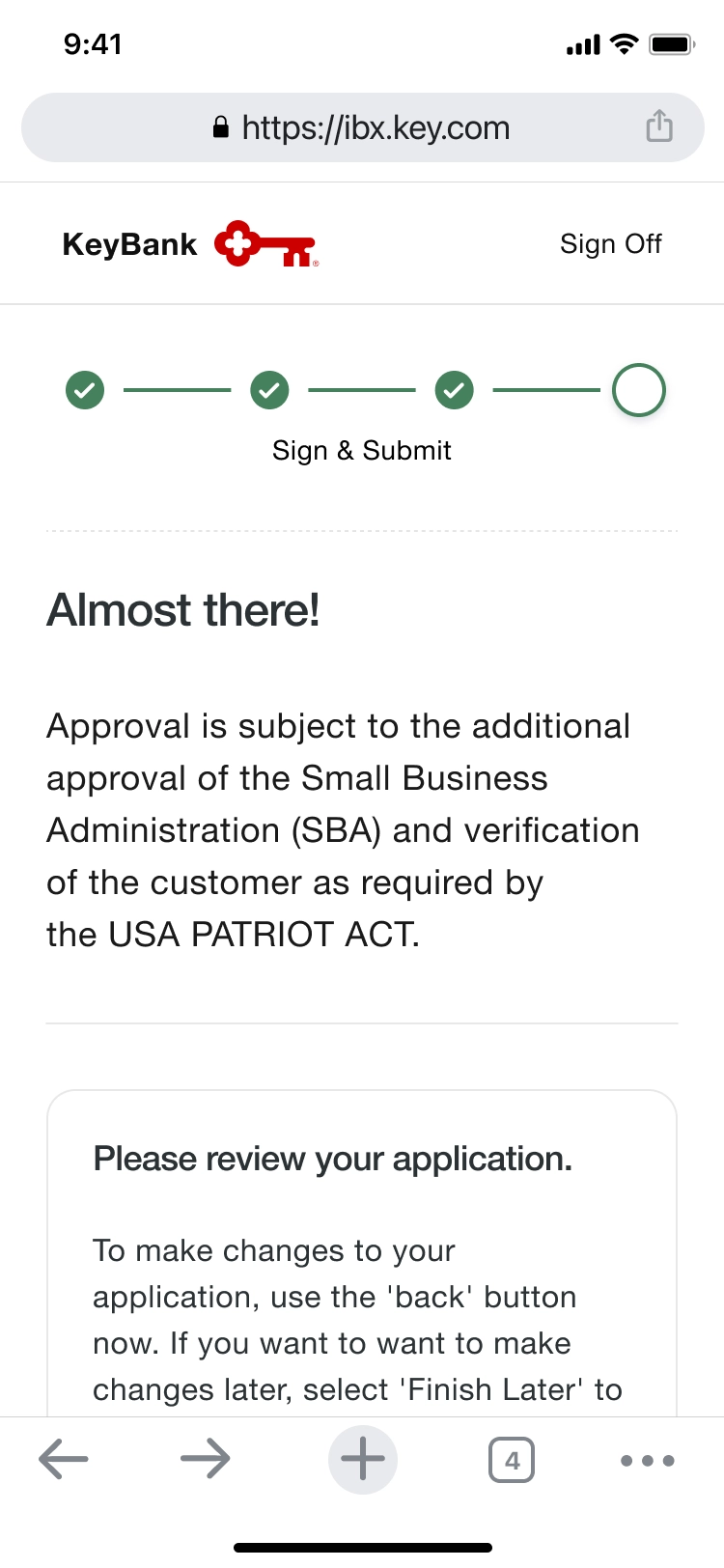

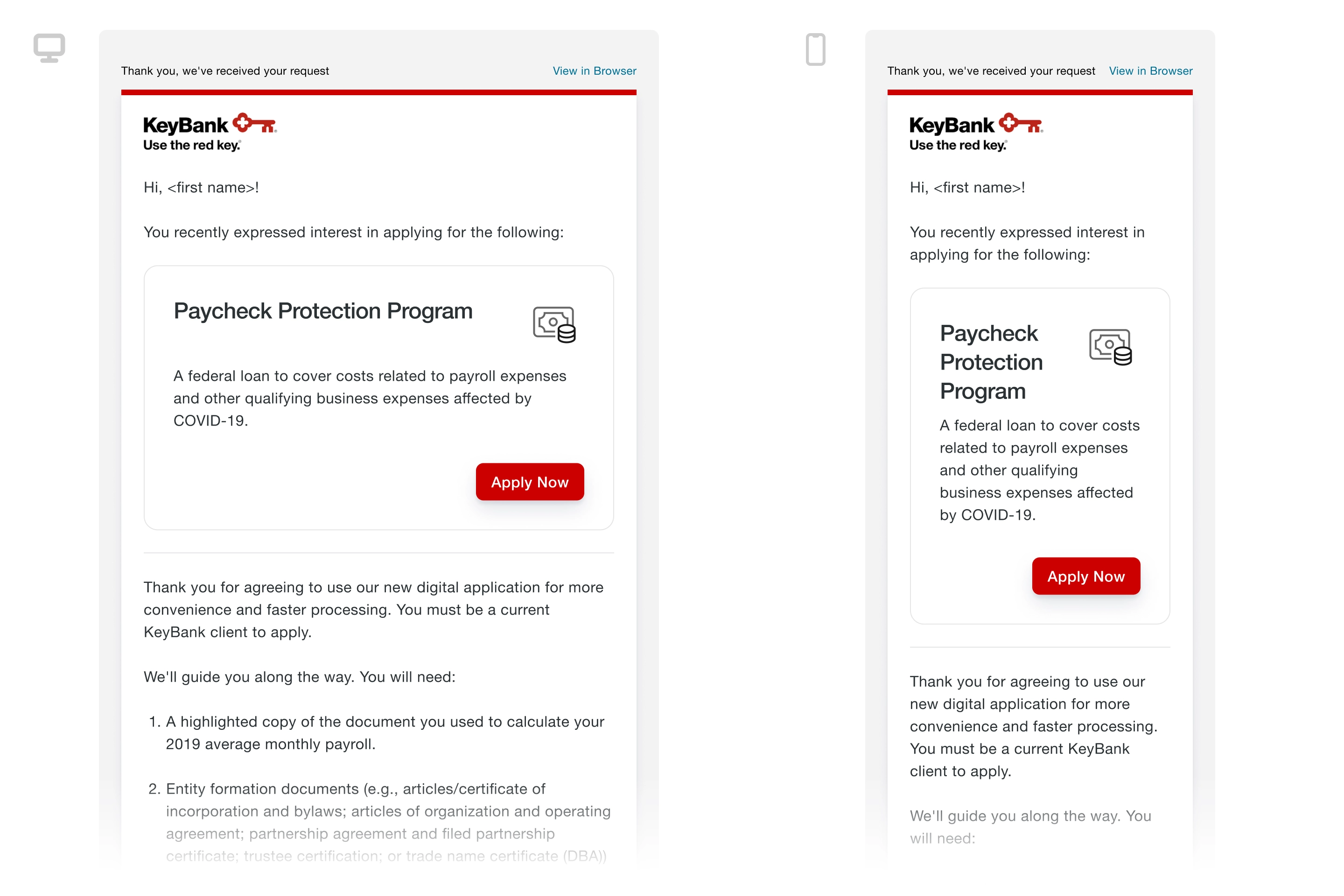

The Paycheck Protection Program is a federal loan intended to help thousands of businesses quickly gain funds. These funds help cover certain business costs related to payroll expenses, the continuation of group health care benefits, lease payments, mortgage interest payments, utility payments, and interest on other pre-existing debt obligations.

I was the only designer joining a core team of business and technology to convert SBA Paycheck Protection Program Borrower Application Forms into a digital experience to streamline the underwriting process and expedite review and approval for funds for our small business clients.

Notable deliverables include: wireframes, interactive prototypes, user acceptance testing, data analysis of system user feedback on OpinionLab, a Software as a Service (SaaS) product